Blockchain technology can be considered a special kind of safe digital notepad for information recording. This notebook is shared among many users, making it hard to change the information without everyone knowing. Originally, it was created for digital money like Bitcoin, but blockchain is now used in many other areas too. Let’s explore what blockchain is and how it works.

Blockchain is a shared digital ledger that can only be altered with the consent of all involved, making it virtually impossible to manipulate data.

It was originally designed to work with cryptocurrencies (like Bitcoin) but is being used in a lot of other things today.

Blockchain works by linking blocks of data in a chain, making it very hard to change any information.

There are three types of blockchain: public, private and consortium blockchains.

Apart from money, the application of blockchain technology goes much further in every field relating to supply chain management, healthcare, or even finance.

Understanding Blockchain Technology

Definition and Basic Concepts

Blockchain technology is a structure in which records of transactions are stored. Also, called the block, of the users in the various databases, called the chain, in a network connected through peer-to-peer nodes. The owner’s digital signature authenticates each transaction, ensuring its authenticity and safeguarding it against tampering.

How Blockchain Differs from Traditional Databases

Blockchain

Traditional Database

In Blockchain, there is no single point of control which means it is decentralized.

In Blockchain, the records cannot be altered which ensures data integrity.

Blockchain is transparent and more secure.

The data in traditional database can be altered.

Traditional databases are less secure as compared to blockchain

Traditional database are less secure as compared to blockchain

Blockchain maintains full confidentiality

Traditional database is not fully confidential.

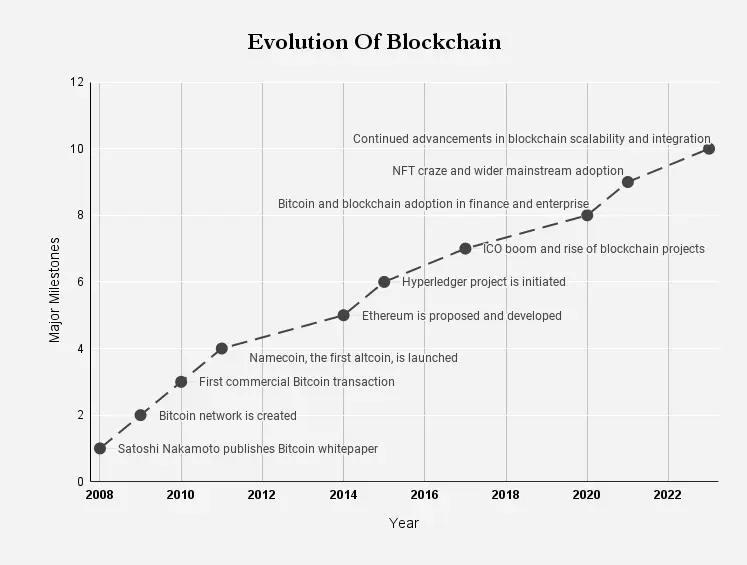

The History of Blockchain

Origins of Blockchain

In 2008, the mysterious Satoshi Nakamoto introduced blockchain to humankind for the first time. Implemented the next year as part of Bitcoin’s core protocol, it is a digital ledger for securely recording all transactions on the bitcoin network. The blockchain technology has improved a lot since then, and it is no longer limited to the realm of cryptocurrencies; you can even find use cases in industries such as supply chain management, healthcare or finance.

Evolution Over Time

Until 2009 Blockchain technology had been little more than a full theoretical concept. Bitcoin employed blockchain to record all transactions in a manner that was safe and transparent. This has seen many other applications come into being since, each showing different aspects of blockchain technology.

Major Steps in Development of Block Chains

2009: Bitcoin emerges as the first use of blockchain technology for cryptocurrencies.

2015: Ethereum undertakes and brings smart contracts in front of the world of blockchains.

2020: Decentralized Finance (DeFi) gained traction and provided a new use case for blockchain

How Blockchain Technology Works

The Role of Nodes

A single computing device that participates in the blockchain network is called a node. Every node contains a complete copy of the blockchain making it both transparent and secure. Additionally, nodes are used to confirm and validate transactions which helped build a decentralized network that shortens the blockchain entirety.

Consensus Mechanisms

In distributed computing, consensus mechanisms are protocols used to achieve agreement on a single data value among nodes of processes. Also, they provide a consensus on valid transactions across all network nodes.

Mining and Validation

Mining involves adding transactions to the blockchain. Miners tackle challenges to verify transactions and incorporate them into the blockchain. Maintaining the blockchain’s security and integrity is aided by this procedure.

Fundamentally, a blockchain plays a role in sharing database or ledger where the information/record/data is stored in the form of blocks with each node possessing a copy of the blockchain. This setup promotes transparency & security throughout the network

Types of Blockchains

Public Blockchains

Private Blockchains

Consortium Blockchains

Blockchains are accessible to all individuals.

Private blockchain have limited access, only some users can become the network’s part.

Consortium blockchains represent a combination of private features, controlled by a group of organizations rather than a single entity.

These blockchains operate in a manner that enhances security features for cryptocurrencies such as Bitcoin. The transparency of blockchains allows for transaction visibility for anyone.

Businesses use these types of blockchains frequently for operations , offering more control and more privacy in comparison with their counterparts.

This type is commonly employed in industries requiring collaboration among entities like supply chain management.

Understanding the distinctions among types of blockchains aids, in selecting an option that aligns with our requirements. Blockchain is of three types:- consortium, private and hybrid. More and more categories of blockchain are emerging within the realm of permissioned or permissionless blockchains.

Key Components of BlockchainTechnology

Blocks and Chains

As the name suggests, a blockchain is just a chain of blocks where each block contains some data and links to previous transactions. Each block includes a list of transactions, and when that block is completed, it can be added to the chain in an unbroken chronologic sequence. This design warrants the storage of data with security and transparency.

Cryptographic Hashing

In cryptographic hashing, you take some input and output a fixed length of string using characters that seem random. This hash is unique to the input data and if you modify this value in any way, there will be a new and completely different hash for that modified file. This effectively makes the blockchain tamper-safe because if anyone wants to change even a single part of that information then they have to make changes to every hash associated with all next blocks.

Smart Contracts

A smart contract is a self-operating contract with the terms of the agreement written into code. They automatically enforce and carry out the terms of the contract after a few requirements are met. It gets rid of the necessity for intermediaries and it guarantees a clear way to carry out transactions.

Having such ideas in mind makes us realize the blockchain and subsequently, how this amazing technology keeps it safe for a real transparent transaction space.

Blockchain in Cryptocurrencies

Bitcoin and Blockchain

Do you know? Bitcoin was the first cryptography that saw the opportunity and took blockchain technology in its favor. Cryptographic hashes provide a safe connection between blocks, or transaction records, to create a distributed ledger known as a blockchain. This list of blocks is constantly expanding. This makes changing old transactions almost impossible. This is due to the fact that Bitcoin runs on a public blockchain, which is an open, dispersed ledger that anybody can access.

Ethereum and Smart Contracts

Ethereum performed exponentially better by adding smart contracts to the blockchain. These are smart contracts that can automatically enforce the agreed-upon terms because they have them written into code. This makes transactions automatable and less dependent on trust. Additionally ,decentralized applications (dApps) are supported on Ethereum’s blockchain which can run without any possibility of downtime or censorship.

One of the most recognizable blockchain technologies is Bitcoin itself – a decentralized digital currency using DLT that has completely redefined how people think about transactions and ownership online since it first arrived.

Applications Beyond Cryptocurrencies

Supply Chain Management

Transparent, decentralized and secure data management of blockchain is helping out a number of industries to transform. It ensures the traceability and authenticity of products from origin to consumer in supply chain management. This transparency helps reduce errors, and frauds, strengthens trust among stakeholders and improves inventory management

Healthcare

Blockchain in Healthcare: Patient Record Privacy and Integrity Seamless sharing of medical data with authorized parties, which can lead to better patient outcomes. Additionally, it can help in tracking the supply chain of pharmaceuticals, ensuring that counterfeit drugs are not distributed.

Finance

Blockchain’s impact on this field extends beyond cryptocurrencies. As a result, transactions are made easier and less reliant on middlemen. Smart contracts play a role in automating and enforcing contracts, further increasing the efficiency of the process.

Blockchain technology is revolutionizing industries by offering a transparent and effective method for managing data and transactions.

Security Features of BlockchainTechnology

Immutability

A feature of technology is its immutability. This guarantees that all transactions are permanent and resistant to tampering, which is essential for preserving data integrity and preventing fraud.

Transparency

Blockchain provides a level of transparency. Every transaction is documented on a ledger for all network participants. This transparency fosters. Confidence in the system since everyone can independently verify transactions.

Decentralization

The decentralized nature of blockchain means there’s no point of failure. The network is supported by nodes, making it resilient, against attacks and breakdowns. This decentralization also ensures that no single entity controls the network, promoting fairness and security.

Scalability is one of the biggest burdens blockchain technology is facing. When there is an increase in the number of transactions, issues like inefficiency and network congestion will also arise. This is because every node in the network has to process every other transaction as well as to handle any increased costs or delays.

Energy Consumption

Blockchain networks, particularly those utilizing a proof-of-work consensus method, consume vast amounts of power. This high energy use is a serious problem because it is environmentally damaging. Research on consuming less power is an important focus in the blockchain space, both in R&D and implementation. Regulatory Issues

Regulatory Concerns

Of course, there’s the environment! In general, this is all still under development and may eventually evolve into something like a regular cloud. Different countries have different regulations which creates uncertainty for companies trying to do business with them & for people who develop software products based on their standards. One of the key determinants of how widely blockchain technology is adopted will be overcoming these regulatory constraints.

While blockchain offers many benefits, it’s important to address these challenges to ensure its sustainable growth and adoption.

Future of Blockchain Technology

Emerging Trends

The future scope of blockchain technology will be discussed later, but blockchain is already being leveraged in many industries, and its potential future spans from supply chain management to cloud storage mechanisms, and startups are committed to providing solutions. We all know that blockchain is versatile and can be implemented as a technology virtually in any industry. We expect more and more companies to turn to blockchain for greater transparency and enhanced security measures

Potential Developments

We still have a lot more to see in terms of blockchain technology advancements over the coming years. This might be in the form of making blockchain more scalable, i.e., efficient and faster. Also, it can introduce the development of new consensus mechanisms that would lower power usage another major criticism of blockchain today. Blockchain is combining with other emerging technologies, such as artificial intelligence and the Internet of Things.

The potential of blockchain lies beyond cryptocurrency in helping to build a more transparent and trustworthy digital environment.

Getting Started With Blockchain

Basic Requirements

If you want to start exploring blockchain, then you need three basics. You will still need a strong computer science or mathematics background as your base. This will give you a brief idea of what is fundamentally behind blockchain technology. Moreover, having knowledge of programming languages such as Python, JavaScript or Solidity can be very helpful.

Learning Resources

So many resources are out there to learn blockchain so what is pulling you back! That is where you can find online courses, tutorials and books. There are plenty of websites and universities, like Coursera, Udemy, Khan Academy, etc. that offer dedicated courses on blockchain technology. Those little YouTube videos and community forum posts can go a long way in helping you with your problem.

First Steps Towards Implementation

Once you grasp the basics, It’s time to dive into action. Start building projects that will give you an idea/knowledge/experience. The issue that now needs to be addressed is where to begin. Begin by creating a simple smart contract or blockchain. As a result, one will gain more confidence with increased progress on projects. Keep in mind that mastering blockchain development requires practice.

Commencing your journey with academics is crucial. A solid academic foundation in computer science or mathematics will pave the way for your career as a developer.

Common Misconceptions About Blockchain

Blockchain and Bitcoin Confusion

Many people have a wrong idea about blockchain, they believe that Bitcoin and blockchain are the same thing, which is not true. In simple words, Bitcoin is a financial product made with this technology. BIockchain has other applications as well. Bitcoin is only one application of this technology.

Blockchain Immutability

Some hold the belief that data stored on a blockchain is immutable and cannot be altered. While changing data on a blockchain poses challenges, it’s not entirely impossible. There exist methods to modify or rectify information when necessary.

Blockchain’s Role in Cybersecurity

There’s a misconception that blockchain can resolve all cybersecurity issues. While blockchain does provide security advantages it is not a panacea for all security concerns. Additional security measures are still required to safeguard our data.

Blockchain and cryptocurrency are constantly evolving. There are people who are still discovering the extent of their capabilities.

In summary, blockchain is a powerful technology that changes how we store and share information. It creates a secure and transparent way to record transactions and track assets. By linking blocks of data in a chain, it ensures that the information cannot be changed once it’s added. This makes blockchain very useful for many different industries, from finance to supply chain management. As more people and businesses start to use blockchain, it will likely become an even more important part of our digital world.

Frequently Asked Questions

Q1. What is a blockchain?

Blockchain is a way of recording digital transactions that is difficult to change. New data is written to a block. Each block is linked to the previous one by a digital signature (until they form a chain). Given the information, all other computers in the network can compare their copy against the thus-far ‘official’ one and determine which parts have been changed.

Q2. How does blockchain technology work?

Blockchain technology combines the advantages of secure cryptography and communication between nodes to implement rigorous administration processes and safety measures, to avoid effective centralized manipulation. Current technologies do not yet have a satisfactory mechanism for managing and maintaining trust among multi-person shared systems, thus making it difficult to realize a robust security architecture or significant improvements in trustworthiness.

Q3. What is a blockchain node?

Nodes are the devices that form the junction of a blockchain network. Much like everyday computer terminals your machine is one of these pieces. Their main job is to distribute transactions so that the blockchain itself can be updated and maintained.

Q4. What is cryptocurrency mining in blockchain?

Mining is the process of appending new blocks to the blockchain. Miners solve complex puzzles to validate transactions and are rewarded with new coins.

Q5. What are public blockchains?

A type of blockchain network that anyone can join it, read the data and add new blocks, or a network that has no restriction on input.

Q6. What is a smart contract?

It is basically a contract with the terms of the agreement between the seller and the buyer written into code.It automatically. enforces agreements and rules.

Q7. How is blockchain used in the world of cryptocurrencies?

Blockchain is the technology backbone of cryptocurrencies like Bitcoin. It records and verifies all transactions, ensuring their security and transparency.

Q8. What are the biggest challenges blockchain technology faces?

Blockchain faces challenges such as scalability issues, high energy consumption and regulatory concerns. These call for integration into wider practice.